By Tienlon Ho

I checked listings daily, made spreadsheets of the ones my fiancé Jon and I both liked, and every Sunday we went religiously to open houses. Over the next six months, we found ourselves in line viewing a crumbling craftsman in the Richmond, getting the silent treatment from squatters in Berkeley, interrupting a Muslim family in prayer in Rockridge, and watching sale prices shoot up by hundreds of thousands of dollars in Temescal.

When we started bidding far over asking only to get soundly outbid — in cash — it was time to take stock. Looking around our little apartment, we suddenly remembered all the good things about it. So we decided not to buy a house, at least, not now. And our lives (especially our weekends) have been much happier for it.

Plenty of would-be buyers are coming to the same conclusion after investing a lot more time into eviscerating bidding wars. We feel lucky to have saved ourselves the disappointment, and worse — buyers’ remorse — by first digging deep into these big questions:

How much is this really going to cost?

If you’ve been living in a rent-controlled apartment for a few years, buying a house is likely going to cost more than what you’re paying now. Once you get past the loan fees and 20% down on, say, a $500,000 “starter” home, you’re looking at a minimum of $2,750 a month on just the mortgage (at a 4.5% interest rate), taxes (1.17%, the average in San Francisco), and insurance ($150, again the city average based on value). Add in utilities and upkeep, and realistically you’ll be responsible for shelling out more than $3,000 a month.

Don’t bank on those tax breaks for mortgage interest and home equity debt that everyone always talks about. Once you crunch the numbers, they only make up for a month of costs, depending on your tax bracket.

Applying for preapproval through a bank like Wells Fargo or a local mortgage lender like RPM will give you an idea of what you can afford. Things are easier if you can pay in cash. Duh.

Is the sort of house I want up for sale?

Over the many months that Jon and I looked, only a handful of houses ever went up for sale in our favorite neighborhood. Out of the 70 or so houses we checked out, only a few interested us. Just one excited us.

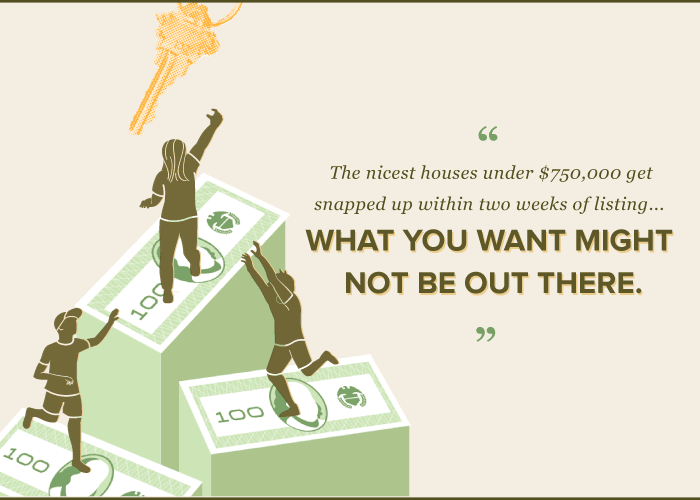

Lots of analysts are saying the Bay Area is in the middle of a housing bubble, meaning there’s very little inventory, low interest rates, and too many people ready to buy — people like start-up VPs and overseas investors pouring cash into real estate (almost a third of sales are to absentee buyers). The nicest houses under $750,000 get snapped up within two weeks of listing.

This has meant in just the past year that Oakland home prices have shot up by more than 31% pushing the median sales price from $240,000 to $537,000. San Francisco’s rose by 20%, bringing the median price to a whopping $1 million. What you want might not be out there.

Where do I want to be in seven years?

Banks will tell you it takes at least this amount of time to make up for all the cash you shell out upfront for your house. So you have to ask, am I ready to commit? That means committing to not only maintaining a house, but to sticking to jobs that pay enough to cover the mortgage, staying in a relationship (if you’re going in with someone else), and dealing with all the unexpected things to come.

A couple I know bought a house with a bonus basement apartment thinking it would be a great place to start a family and make great investment, only to find themselves in a lawsuit with their crazy tenant a year later, followed by said tenant’s suicide, and their own divorce proceedings a year after that. They sold the house at a loss a few years in, and the ex-wife ended up back in their old apartment building — hundreds of thousands of dollars lighter.

Most house-buying stories don’t end this way, but it can be surprisingly tricky adapting your house to even the good things that happen in your life. Neighborhoods are subject to zoning regulations that often prevent tacking on an annex or converting a garage to fit new kids, a big dog, or an overgrown vinyl collection.

How do I feel about paperwork?

There are lots of ways to buy a house without middlemen, but doing so means taking on mountains of paperwork on your own and, more scarily, the risk of overlooking critical information. Despite what real estate agents tell you, handling your own closing is doable. You just need patience for details.

For those with nonlinear career paths or bad credit, a mortgage broker is unavoidable. A realtor is handy if you don’t want to read up on real estate ins-and-outs. In some cases, listing agents will deal only with buyers who have agents, supposedly because they want to make the process go as smoothly as possible.

In the end, most sellers just care about a “competitive” bid (read: high, fast, and certain) — not who makes it.

Where’s the bus stop?

When you start in on the open houses, you’ll be tempted at first by the siren songs of beautiful houses in the middle of nowhere. Don’t let the glint of a sub-zero blind you from the fact that the length of your daily commute can mean the difference between happiness and heart attack.

Less obvious considerations are good schools (even if you don’t have kids, this helps keep resale value up), decent grocery stores, a movie theater (Jon’s requirement), and a library (mine). Also, cellphone reception. No amount of lemons from your very own tree is worth the hassle of balancing on a chair in a closet to look for two bars.

Are those puppies

or attack dogs?

Once you’re seriously considering a house, check it out at all hours of the day, not just during open house hours. If you see blackout curtains, bars, and security cameras on all the neighbors’ windows, consider moving on, or at least budgeting for your own security measures.

We researched houses using online resources like Crime Mapping, sorting out crimes like fraud from the freaky ones like homicide, as well as reading the neighborhood’s local paper and Patch. We also learned to check the disclosures (the packet info you get from the listing agent) for CLUE (Comprehensive Loss Underwriting Exchange) reports, which lay out the insurance claims made on the property. After one adorable ranch on a tree-lined street in Berkeley included a CLUE report listing almost $50,000 in stolen property in just the past year, we made sure to ask for those reports.

What’s under the paint?

Flippers put more effort into hiding things under panels of reclaimed wood rather than actually fixing them, so it can be hard to see the termite-riddled baseboards and layers of roofing unless you know what you’re looking for.

Kick the tires. If more than the outer layer of the foundation crumbles when you kick it, if there are horizontal cracks in any supporting surfaces, if the floors are badly slanted, if there’s a wet, moldy smell, or if the windows won’t open, you could be looking at anywhere from $12,000 to $200,000 in immediate repairs. Also, look for a sagging roof or watermarks indicating leaks that have been painted over, and look at the wiring (insurance companies often won’t insure houses with outdated knob and tube wiring). Bad news, but lots of houses in these parts are just reaching that age when their foundations and electrical systems are due for an overhaul.

Before you commit to buying a house, bring an inspector to check things out. Relying solely on disclosures is an unnecessary risk, especially if the big checks (foundation, roof, sewer, heating, electrical, and pest) are dated or done by a notoriously seller-friendly inspector. A full inspection will cost $400 to $600, and if you get it done before bidding, you can waive the inspection period and speed up closing, which will entice sellers.

Who died here?

Inspection reports are disorganized and full of jargon, but they get comprehensible by your second house. Look at the pest pictures and see how many years the termites had to build their cities. In the East Bay, look for when the sewer lateral line, the pipe that sends your poop out to the city’s sewer line, was last replaced. In the olden days, buyers could negotiate with sellers to get those costs taken out of the sale price. Forget that now, but keep it in mind when deciding what the house is worth to you.

If you believe in ghosts, talk to the neighbors. Sellers are supposed to disclose deaths that occurred in the past three years, but sometimes you have to ask and often they offer wily answers. Unfortunately, in this market, the mass-murder discount isn’t as much as you’d think.

Do I feel happy sitting in the living room?

Buying a house that isn’t quite right is like buying a pair of pants that fit weird in the crotch. You keep thinking you’ll get them fixed, but of course you never do. They languish in the back of your closet, a daily reminder of your laziness. Now imagine having to live in those pants — a pair 10,000 times more expensive.

For really major fixers, the Federal Housing Administrations 203(k) program offers renovation loans at decent interest rates for home owners ready to renovate within six months of closing. Just keep in mind, some sellers hesitate to deal with the potential hiccups that go with buyers dependent on these loans. Also, consider that if you’re the sort of person who quit halfway through making a lamp out of bottles and a bag of concrete, taking on an entire DIY house probably won’t be much different.

Look for a house with good bones and set realistic expectations about the things you’ll change.

Why do I want this house? Wait, why do I

want one at all?

One of the things every real estate agent says when you decide to go for a house is to write a personal letter to accompany your bid. This turns house buying into something like applying for a job. When we were writing the letter for one house, the reasons just flowed. We loved the big windows, the original woodwork, the chicken-friendly yard, and the radiant heating. For another, we struggled to come up with anything specific. When a house is right for you, it’s easy to explain why.

Just make sure your reasons don’t all revolve around the same theme. When owning a house becomes a rite of passage, a mark of being a grown-up, or proof that you’ve accomplished something, it turns into just another task you’re just supposed to check off, not something you really want to do. Give yourself permission to do all the other things you’ve been dreaming of or putting off — regardless of whether you own. After all, a house is just a place to live your life.

If you’re in the market to buy, there are programs on everything from applying for a mortgage to working with an inspector through the San Francisco Mayor’s Office, the City of Oakland, and real estate agencies like Redfin. Be patient. Make generous and responsible bids. And keep your fingers crossed.

The Bold Italic is a not-for-profit media organization, and we publish first-person perspectives about San Francisco and the Bay Area. We operate under a fiscal sponsorship of a 501(c)(3).

You can become a paid subscriber. Or donate. Or learn more about us.